As mentioned in a previous article, at the end of August 2022, Rune Christensen, co-founder of MakerDAO, mentioned the Endgame plan in the article "The road to compliance and the road to decentralization: Why Maker has no choice but to prepare to free float DAI".

Thereby Christensen wants to bring MakerDAO to develop in a sustainable, decentralized and decentralized way. But that will make a big impact on the DAI protocol and the DeFi platforms that rely heavily on this stablecoin, such as Curve Finance.

MakerDAO's Endgame Plan

The goal of the Endgame plan is to improve and develop the protocol to reach a self-sustaining equilibrium to ensure stability and decentralization for Maker in general and DAI in particular, and to protect the protocol from damage. Similar events have happened to Tornado Cash if it continues to depend on USDC.

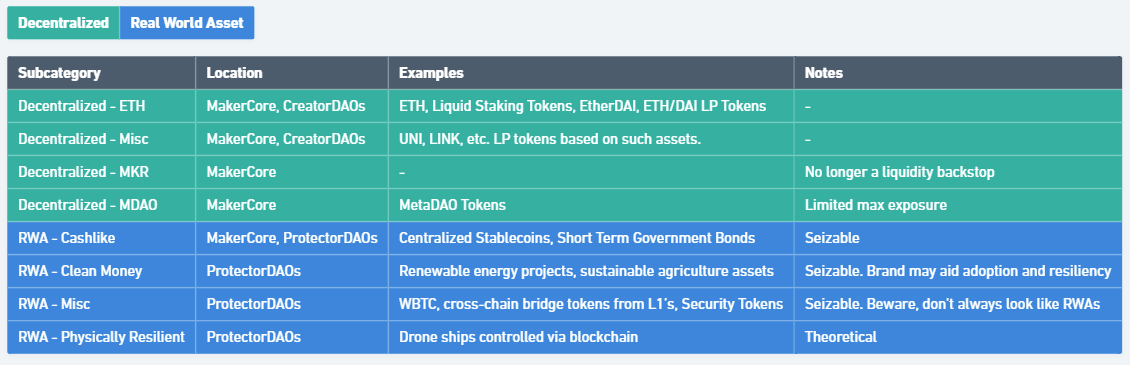

According to the Endgame Plan Full Overview v3, Christensen aims to make DAI a free-floating asset, an "unbiased world currency". With the initial focus on the "international currency" factor when DAI will be collateralized with real-world assets (RWA - Real World Assets), there is no limit on the risk level of RWAs and continued to maintain a 1:1 exchange rate between DAI and the dollar for about 3 years.

Then move to focus on the objective factor by allowing the DAI to deviate from the peg and hard limits for the collateral's relevance to the RWA must be set.

Because RWAs are based on the traditional financial system, where regulators can take advantage of this alignment to regulate or eliminate the viability of a crypto project. So when Christensen mentions risk reduction from RWA, it is conceivable that there is a need to reduce investments/collateral that are seized or frozen by regulators. At the same time increasing the decentralized collateral collateral for DAI. Thereby increasing the sustainability for Maker.

Rune believes that the only way to guarantee a hard limit on the relevance of collateral to RWA is to release DAI. If DAI fails to meet demand through decentralized collateral, the loss of the peg will be inevitable. And to support successful floating DAI is supported by two of two tools:

- MetaDAO and MetaDAO tokens: MetaDAO creates a decentralized economy run by decentralized organizations that are not controlled by authorities. Yield Farming from MetaDAO will be a key factor to incentivize the creation of more DAI from decentralized collateral, incentivizing users to hold and use DAI.

- Protocol Owned Vault: A strategic protocol that enables Maker to accumulate large amounts of Staked ETH on their own with leverage and thereby control the minting of large amounts of over-collateralized and fully decentralized DAI.

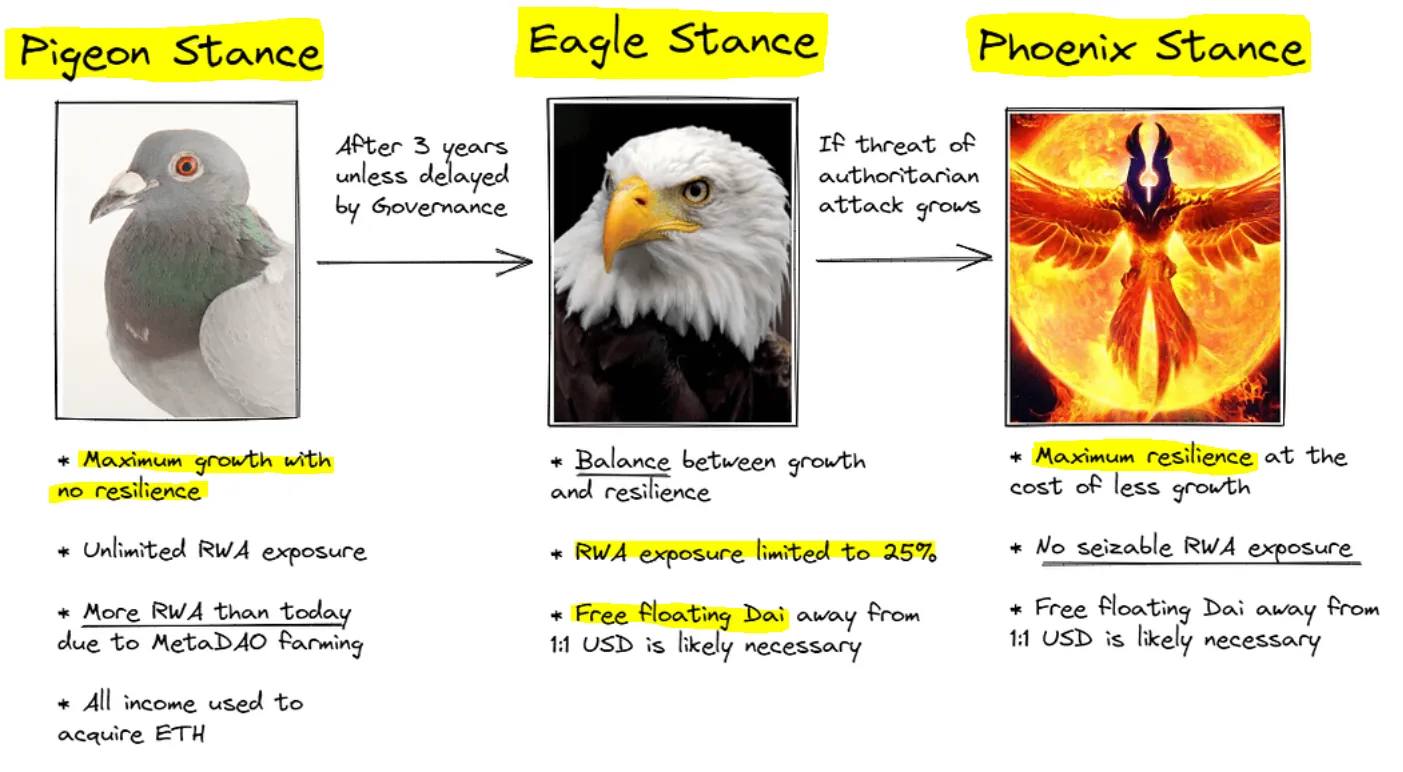

The DAI floating plan is outlined with 3 states:

Pigeon Stance:

- Maximize growth and ignore sustainability.

- No limitation regarding RWA of collateral.

- Any revenue will be used to buy more ETH.

- It is expected that this state will be maintained for 3 years and move to the next state if there is no change from the DAO

Eagle Stance:

- Balance between growth and sustainability.

- Set collateral RWA-related limit at 25%.

- Floating DAI from USD may be necessary.

- And if the protocol is at risk of being threatened by the next state regulators, it will be deployed.

Phoenix Stance:

- Maximizing sustainability at the expense of less growth potential.

- Ensure no RWA assets can be seized by agencies.

- DAI will probably be floated.

In short, DAI will continue to maintain a 1:1 exchange rate to the dollar for at least another 3 years. A free-floating DAI is likely to happen, but it is uncertain and difficult to predict precisely because it depends heavily on the future regulatory environment.

Leverage for current $DAI supply and demand

Before going into the effects this new mechanism may have on other liquidity platforms, we need to have an overview of the main drivers that help to stabilize the state of supply and demand:

- DSR (DAI saving rate): the rate of return users receive when holding $DAI (rewards are extracted from Surplus Buffer). If this rate increases, it will stimulate the demand for $DAI.

- PSM (Peg Stability Module): allows users to directly swap a certain stablecoin to $DAI at a fixed rate. For this form, the user is not obligated to repay the debt to redeem the stablecoin mortgage, simply a swap transaction ⇒ helps to stabilize the DAI peg but also creates associated risks for Maker when holding. many stablecoins (centralized collateral - potentially subject to legal or some other regulatory impact).

- SFBR (Stability Fee Base Rate): The interest rate for a leveraged position. Increase in interest rates ⇒ fewer borrowers ⇒ decrease in supply (extra $DAI mint).

Effect of floating $DAI on liquidity of $DAI and derivative $DAI tokens on Curve

Once $DAI is floating, the $DAI value will not be fixed 1:1 USD as before but depends on supply and demand. So what happens when the value of $DAI drops? At this point, investors will tend to sell $DAI at the best possible price and get back their collateral. In this case, there will be a price difference between the DAI liquidity pairs with the DAI buying price at PSM ⇒ an opportunity for traders to benefit from the arbitrage.

If through PSM, because the rate is fixed, $DAI decreases, which means that other stablecoins will also decrease in value accordingly. Instead, they will choose liquidity pools and withdraw USDC or USDT in exchange for DAI before the ratio equalizes, resulting in 3pool holding a large amount of $DAI. USDC & USDT liquidity will be drained⇒ affecting USDC/USDT exchange rate as well as increasing Impermanent Loss.

A solution is proposed based on the current conditions as follows:

Separate $DAI from 3Pool ⇒ establish a basepool (USDC&USDT) and a meta pool (USDC&USDT)DAI. Hence, the centralized liquidity of USDC+USDT can be adjusted independently of the $DAI metapool. This also solves the problem of exhausted liquidity because the amount of assets required to bring the ratio to PSM will be lower.

In addition, floating DAI will also have an impact on the derivative $DAI token. If the value of $DAI decreases, the borrower only needs to pay a lower amount than the original value to recover his mortgage (same amount of $DAI tokens but lower value because of the decrease in the price of $DAI) going Borrowing in this case is very profitable, so it is possible that the borrower will repeat the sequence of actions - depositing collateral and borrowing $DAI, as long as the amount of collateral remains liquid. Each time the price of $DAI falls, more $DAI can be borrowed ⇒ indirectly reducing the price of $DAI because of the large supply to the market. In addition, the lender may face the possibility of not recovering the $DAI they provide because the borrower did not close his position before such a "lucky" deal.