GammaSwap is built with the extremely intelligent Gamma Staddle strategy to profit from the Impermanent Loss risk faced by most liquidity platforms. The project is about to be deployed on Arbitrum - the ecosystem that has been attracting cash flow recently - so this could be a hidden gem for the upcoming growing season. Let's find out with Holdstation through the following analysis.

Currently, GammaSwap is releasing a testnet, to experience the product you can read a detailed tutorial: Guide for Doing Testnet GammaSwap For A Chance To Receive Airdrop From Arbitrum Ecosystem

Since GammaSwap implements a strategy from traditional financial markets to DeFi, before we can understand GammaSwap's operating model, we need to understand some of the following terms.

What are a long straddle and a short straddle?

Option contract

An option contract allows the buyer of the contract to own the right to buy or sell an underlying asset at a fixed price (the strike price) for a specified period of time.

There are 3 numbers to note:

- Contract Purchase Fee - the cost of purchasing a contract.

- Strike price - the price the asset can be bought by the holder of the contract (which is pre-negotiated in the contract). The option buyer will have the right, but not the obligation, to buy or sell the asset in the future at the strike price.

- Actual price - the market price of the asset.

For example, for a call option, you buy an option to call a stock with a strike price of $10 in the next 1 month and pay a premium of $1. The current stock price is $12 and after 10 days the actual stock price has increased to $20. At this point, you have the right to buy this stock at the price of $10 as specified in the contract, and then make a profit from selling the stock at the market price of $20.

Profit = Actual Price - Strike Price - Contract Fee = $9 ⇒ The higher the actual price of the stock, the bigger your profit on the option.

The contract seller will suffer a loss in this case when he has to buy back the stock for $20 when the actual price is only $10. Loss = Actual Price - Strike Price + Contract Selling Fee = -$9

So if you buy Call Option but the price drops sharply ⇒ the biggest loss the buyer has to bear is the contract purchase fee.

And similar to the put option contract (Put Option), at this time the expectation of the contract buyer is that the asset price will drop sharply, so he will buy a Put Option that allows the right to sell the asset at the strike price. For example, the exercise price is $10, the contract price is $1, and the actual price drops to $5, then the owner of the contract can buy the asset for $5 in the market and then sell it back to the seller of the contract for $10 to make a profit. profit $4 (after deducting contract fees).

⇒ The greater the volatility, the more profitable the contract holder.

There will be two objects involved in this transaction:

- Buyer - the party who buys the option contract: Expects the price to move sharply in the predicted direction.

- Writer - the seller of the option contract: Expects little price volatility and profits from the contract's selling fee.

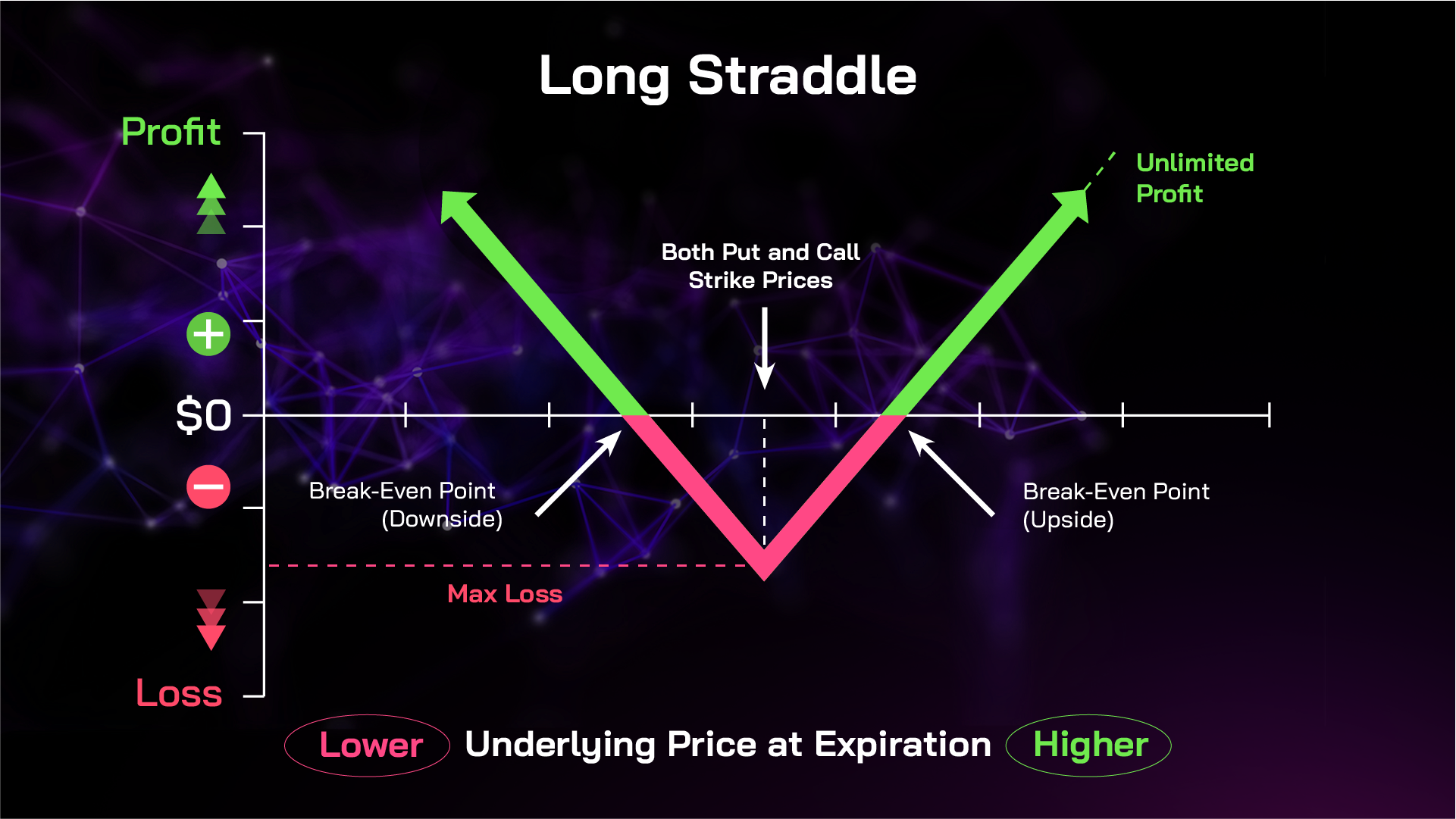

Long Straddle Strategy

If you buy an option contract, you will face the risk of market movements in the opposite direction, so to hedge your trade, investors proceed to buy Call Option and Short Option at the same time for the same. underlying asset and strike price at breakeven - Long Straddle strategy.

To make it easy to understand, because the contract is optional and you have the right to exercise it or not, when you buy both a call and a put contract, you are betting that the market will fluctuate wildly and in any way. Either way, you will still make a profit, as long as the volatility is large enough to cover the cost of buying two contracts. Call options benefit when the price moves up and put options when the price moves down.

For example, if you buy Call Option and Put Option at the same time with the same strike price of $10, the cost for each contract is $1, so the total will be $2. If the actual price during the contract period rises sharply to $20, you will exercise the call (no need to exercise the Put Option) and make a profit = $20 - $10 - $2= $8. And vice versa in case the price drops sharply for the put option contract.

However, if the price only fluctuates in the $8 - $12 zone, an investor can only break even or lose money because the volatility does not cover the cost of buying 2 contracts ⇒ the buyer expects the price to move with a small margin. strength.

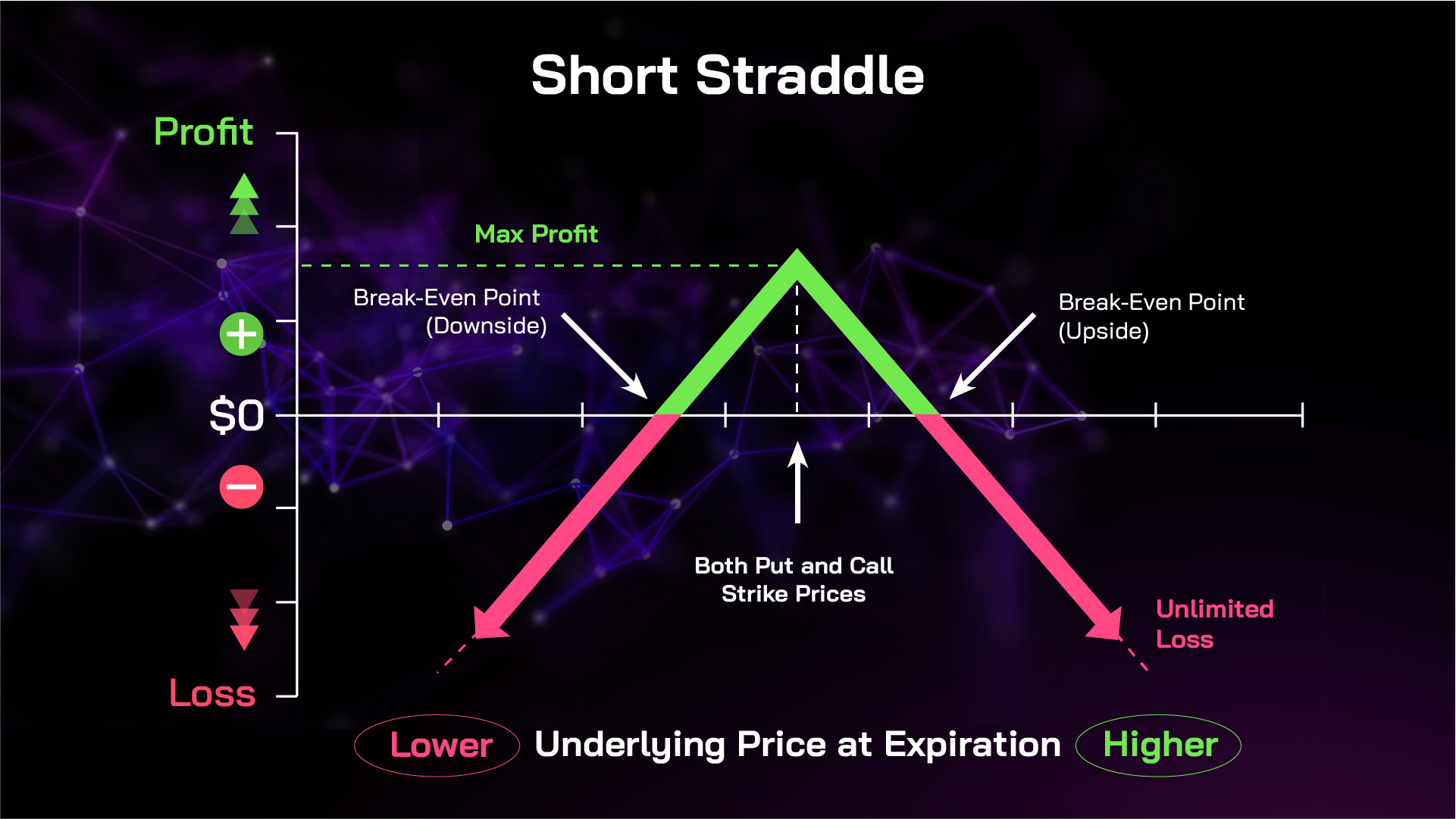

Short Straddle Strategy

So in case the price range is narrow, how to make a profit? At this time, the Short Straddle strategy is applied to the seller of the contract. The writer will expect the market to move sideways in a narrow price range, so he will sell both call and put options at the same time and profit from the cost of selling the contract (instead of benefiting from the volatile price of the contract). Long Straddle strategy as buy-side).

For example, the Writer sells two Call Options and Put Option contracts at the same time with a strike price of $10, each contract worth $5 should earn $10. If during the contract period, the price only increases to $12 and the buyer executes the Call Option. At this time, the seller receives a profit = Strike price (repurchased from the contract buyer) - Actual price (sells to the market) + contract selling fee = $8

Thus, if the market is forecasted to be strong or weak in the future, no matter which direction it moves, investors can still exploit it to make profits in two different positions - Buyer and Writer.

How is this strategy applied by GammaSwap in the DeFi market?

Operation Model of Gamma Swap

The problem of AMM in today's DeFi market

One of the activities of creating passive income in the DeFi market is to provide liquidity and many projects have been developed that play an important role in an ecosystem such as UniSwap, PancakeSwap,... By providing its assets to create liquidity for a trading pair on the DEX, the provider will receive trading fees as well as reward tokens from the platform.

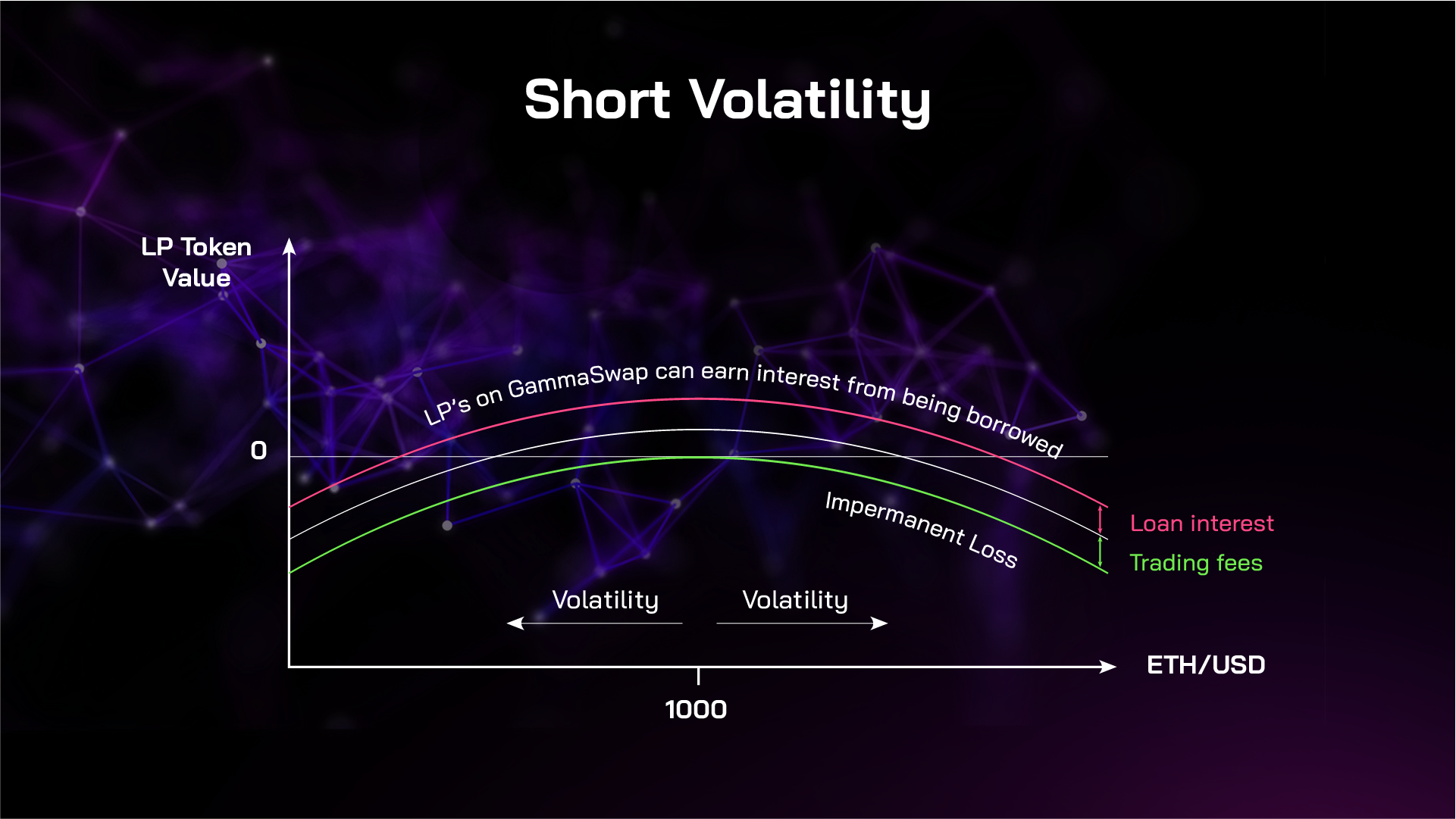

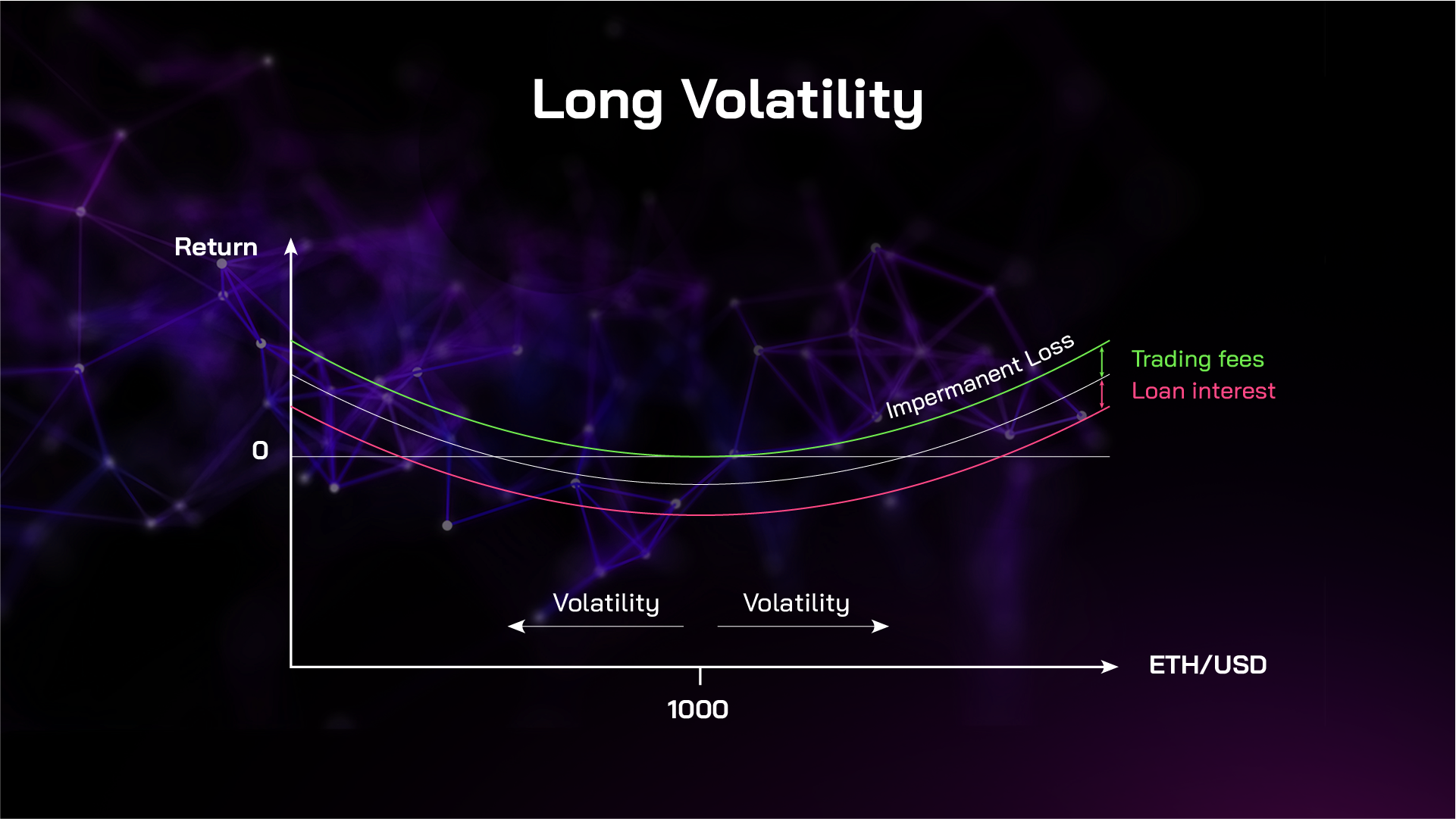

However, the biggest problem of most AMM (Auto-Market Maker) models today for liquidity providers (LPs) is the risk of Impermanent Loss. The more volatile the market, the bigger the IL and LPs are betting that the fee received will be larger than the IL (narrow range market) so it can be profitable.

LPs profit = Trading fees received from the platform - Impermanent Loss

However, if you want high transaction fees, the transaction volume will increase, and the larger the transaction volume, the higher the IL will increase, so in the long term, the profit LPs received will be low or lost.

⇒ Short Gamma (short straddle) LPs with perpetual duration - the same liquidity provider as the option seller.

So where is the Long Gamma side? Currently, there is not. Therefore, Short Gamma is not paid the "contract sale fee". And GammaSwap is the first platform that will create a two-way market for both Long Gamma and Short Gamma. From there, investors can flexibly deploy a hedging strategy to suit each volatile market condition.

Operation Model of GammaSwap

GammaSwap is an oracle-free volatility exchange that creates a market for both Long Gamma and Short Gamma.

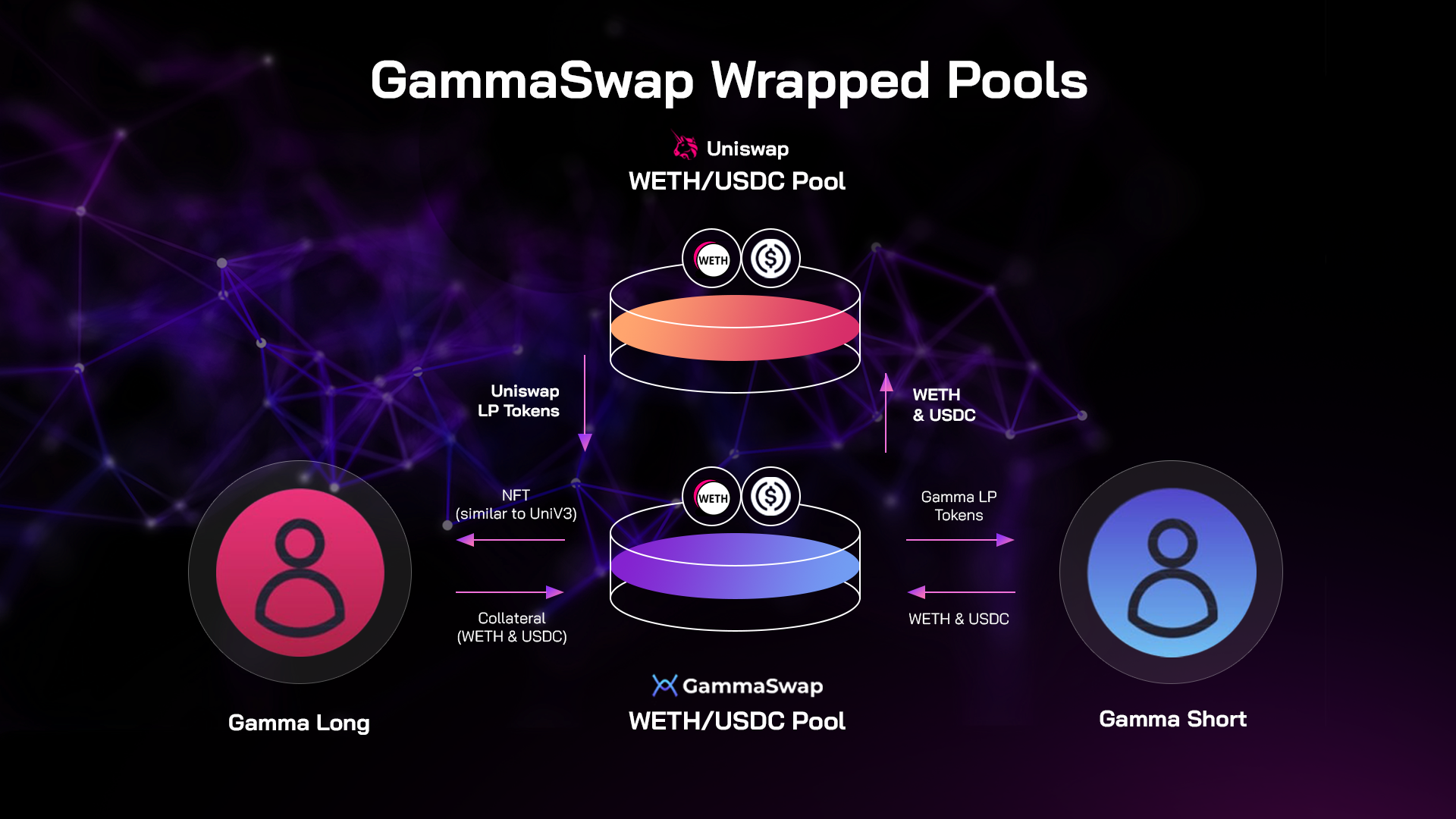

Wrapped Pools

This is GammaSwap's first product. Two objects participating in this model include:

- Short Gamma (LPs) - liquidity provider

- Long Gamma - liquid borrower

Take the ETH/USDC pool as an example. For Short Gamma , which is similar to providing liquidity, LPs will create a position by:

- Deposit the ETH/USDC reserve token pair directly into the GammaSwap (GS) pool.

- Or deposit Uniswap Liquidity Provider token (this is the token you receive when providing liquidity on UniSwap to prove your position) to GS.

If the LP sends the reserve token pair to the GS pool, GammaSwap will transfer this to Uniswap and receive the LP token. Also, mint the GS-LP token for Short Gamma party to represent the position.

⇒ GS holds LP tokens in Smart contract. The gamma short party receives a GS-LP token representing its position at GS.

The GS-LP token is similar to the Uniswap LP token but the difference is that the GS LP will receive an additional interest from the liquid borrower (Long Gamma).

Uniswap P&L = transaction fee - IL

GammaSwap P&L = transaction fee (from Uniswap) + interest received from Long Gamma - IL

⇒ Short Gamma Profit on GammaSwap Profit from UniSwap

So what does GammaSwap hold LP tokens for? It is for the Long Gamma party to borrow.

For the Long Gamma party, in order to borrow an LP position (the LP token has recorded the price information at the time of providing liquidity, it can be considered as a strike price) they will mortgage a reserve token pair to GS and get NFT similar to Uniswap V3 for debt management and representation.

When a user opens a Long position, GammaSwap will return Uniswap LP tokens to Uniswap in exchange for the base token as well as monitor the transaction fees received if still holding Uniswap LP tokens and the loan interest ⇒ these two amounts on the Long side. Gamma will bear to hold his position.

Loan to Value (LTV) ratio, up to 90%. If the value of the loan exceeds this threshold, the loan will be liquidated. The liquidation fee is 5% and all fees from the liquidation will be seized by the protocol's treasury in order to further the development of the protocol.

If the underlying token price fluctuates sharply in any direction (up or down), the loan becomes over-collateralized (e.g. depositing $200 to borrow $100 worth of assets) so the Long Gamma side has can buy tokens at a cheaper price to repay the loan and profit from the difference after deducting the holding fee ⇒ Impermanent Loss becomes Impermanent Gain for Long Gamma.

For example, a liquidity pool currently contains 100 ETH and 10000 USDC with 1 ETH = $100. Long Gamma deposits ETH & USDC collateral to borrow a position providing 10% pool liquidity of 10 ETH and 1000 USDC respectively. If the ETH price increases to $200 ⇒ The number of tokens in the pool will now be 70.7 ETH and 14142.1 USDC ⇒ The loan position is now 10% pool corresponding to 7.07 ETH and 1414.4 USDC ~ worth $2828.4. Your initial position is now worth = 10 x 200 + 1000 = $3000 but now just return $2828.4 ⇒ The profit received is the difference minus the holding fee. The maximum loss Long Gamma incurs is the transaction fee and interest on the loan.

Thus in a highly volatile market Temporary high volatility Profits received by Long Gamma will increase, leading to an increase in demand for Long Gamma Demand for loans increases, so Short Gamma - LPs will also receive interest rates higher.

Summary:

- Short Gamma will get returns at least equal to or higher than other platforms with a similar trade - providing liquidity.

- The Long Gamma pattern becomes a hedge for LPs in a volatile market. However, in order to fully exploit the profits from this form, it is necessary to understand the mechanism and good calculation ability, so it will be more suitable for professional traders.

- Because the value of the mortgage and the debt will be based on the same CFMM (Constant Function Market Maker - AMM uses a constant mechanism like Uniswap2, Pancakeswap,...) the ratio in the CFMM will be the reference price needed. single setting. Since then GammaSwap does not use external oracles, so it will reduce the rate of manipulation and profiteering by unusually large transactions, we can take the recent Mango Market hack as an example with a loss of up to 100 million USD.

- In addition, the project also builds on Non-upgradable SmartContract - Smart contracts cannot be modified, so it can limit the case of taking advantage of security holes to modify smart contracts and make profit.

- The risk from this model, if any, will come from a vulnerability in the smart contract. Currently, the project has not been audited, but according to the announcement, GammaSwap is contacting the audit organization @HalbornSecurity to implement this process.

Currently, GammaSwap is releasing a testnet, to experience the product you can read a detailed tutorial: Guide for Doing Testnet GammaSwap For A Chance To Receive Airdrop From Arbitrum Ecosystem

Other products in the development roadmap

Native Pools

In the future, GammaSwap will build GammaSwap's own liquidity pools instead of through another AMM. The liquidity providers will directly deposit funds into the GammaSwap AMM, thereby profiting from the interest that users holding Long Gamma positions (Liquidity Borrowers) are paying to maintain those positions (instead of that). because of transaction fees).

Feeless DEX - The DEX has no transaction fees

Since GammaSwap Pools do not require transaction fees to incentivize liquidity, the protocol is able to issue a zero-fee DEX to maximize the positions of volatile traders. If this no-fee DEX were connected to liquidity aggregators like 1inch, for example, it would attract a significant portion of small-volume trades - with fees accounting for most of the transaction costs. Thereby increasing market share in terms of users as well as transaction volume.

Although there is no DEX transaction fee, GammaSwap can still generate revenue from the cost of managing Long Gamma positions - specific numbers have not been announced.

Vaults

Besides, GammaSwap will also offer Vaults as a solution to automate strategies for hedging from Impermanent Loss and automatically rebalancing positions providing liquidity based on preset parameters.

These Vaults can work with any type of AMM and centralized liquidity solutions. At the same time, these Vaults will also be used to cooperate with other protocols to build product systems, or ecosystems.

Tokenomic

Currently, the team has not released detailed information, but if the project token is to grow well, Holders should be able to allocate project revenue as well as create more applications - payment of transaction fees, .. - in addition to management rights. treat.

Tokenomics coming soon, we have plans to be way more than just a governance token!

— GammaSwap 🦇🔊 (@GammaSwapLabs) November 29, 2022

Development team

- Daniel Alcaraz Morales (CEO): Graduated from New York University. He has extensive experience in the financial markets in general as he previously worked as an analyst at Goldman Sachs, capital management and electronic trading at investment bank Oppenheimer&Co and algorithmic trading at UBS. As well as crypto trading experience from 2016 to the present.

- Devin Goodkin (COO): Before founding GammaSwap with the other 3 members, Devin worked at the development department of Figment - a company providing staking services.

- Godwin Woo (CTO): Has 12 years of experience working as a programmer at KPMG (An auditing organization in Big4) and investment bank UBS.

- Roberto Martinez (CPO): A young member of the founding team. Currently continuing to study at Florida International University, majoring in computer science. Experienced software engineer internship at Meta (Facebook) and TechStart.

⇒ The team has high expertise and experience, so it is possible in the future to continue to develop more new trading strategies for GammaSwap. Currently, the project is also actively encouraging and communicating with the community about trading strategies that show a high probability of building innovative products.

Conclusion

GammaSwap is currently deploying a testnet on the Arbitrum system and is expected to have the mainnet by the end of January 2023. With a unique model, this can be a channel to leverage good capital in the DeFi world. If the market situation is not as volatile as it is now, then Short Gamma may be preferred at first.

Holdstation Wallet - Your Gate to Web3 💜🦈

Make DeFi as easy as CeFi!

📲 Download now: IOS | Android

Disclaimer:

The information, statements and conjecture contained in this article, including opinions expressed, are based on information sources that Holdstation believes those are reliable. The opinions expressed in this article are personal opinions expressed after careful consideration and based on the best information we have at the writing's time. This article is not and should not be explained as an offer or solicitation to buy/sell any tokens/NFTs.

Holdstation is not responsible for any direct or indirect losses arising from the use of this article content.